ZeroHedge reports that Michael Burry Warns Weimar Hyperinflation Is Coming. Michael Burry is an investor, well-known for being one of the first to foresee the subprime mortgage crises of ~2007-2010.

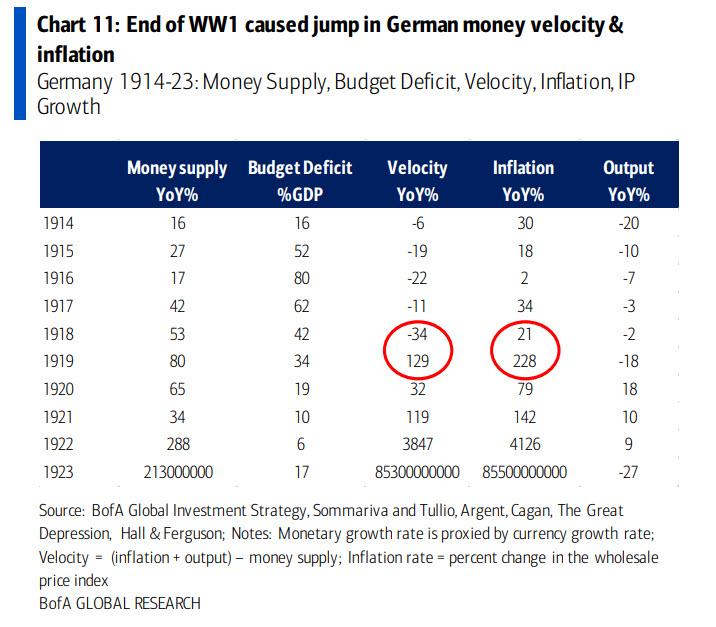

One week ago, Bank of America hinted at the unthinkable: the tsunami of monetary and fiscal stimulus, coupled with the upcoming surge in monetary velocity as the world’s economy emerges from lockdowns, would lead to unprecedented economic overheating… or rather precedented as BofA’s CIO Michael Hartnett reflected back on the post-WW1 Germany which he said was the “most epic, extreme analog of surging velocity and inflation following end of war psychology, pent-up savings, lost confidence in currency & authorities” and specifically the Reichsbank’s monetization of debt, and extrapolated that this is similar to what is going on now.

There is, of course, another name for that period: Weimar Germany, and because we all know what happened then, it is understandable why BofA does not want to mention that particular name.

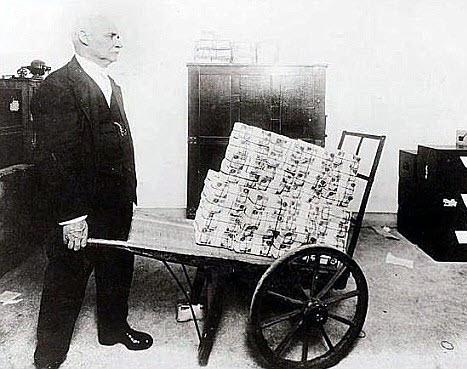

Of course, others have been less shy – in 1974, Jens Parsson wrote a fascinating, in-depth historical analysis of the hyperinflationary collapse of Weimar Germany under the original money printer, Rudy von Havenstein, “Dying of Money: Lessons of the Great German and American Inflations” one which we periodically remind readers is absolutely critical reading in preparation for what comes next.

Is Ben Bernanke The Second Coming Of Rudy von Havenstein, The Central Banker Responsible For Germany’s Hyperinflation? http://bit.ly/bKVeU3

— zerohedge (@zerohedge) February 26, 2010

Then overnight none other than the Big Short, Michael Burry, who has been rather busy making waves within the financial community with his hot takes (most recently, his slam of Robinhood and his bullish view on Uranium), picked up on the theme of Weimar Germany and specifically its hyperinflation, as the blueprint for what comes next in a lengthy tweetstorm cribbing generously from Parsson’s seminal work. And while the details are familiar to most monetary historians, the fact is that now none other than the man who was made famous in the Big Short is calling for Weimar-style hyperinflation in the US. Below is an easily digestible repost of Burry’s lengthy Saturday tweetstorm, which shows just how similar our world is to that prevalent in the years just before Weimar Germany saw the most explosive hyperinflation in history.

The US government is inviting inflation with its MMT-tinged policies. Brisk Debt/GDP, M2 increases while retail sales, PMI stage V recovery. Trillions more stimulus & re-opening to boost demand as employee and supply chain costs skyrocket. #ParadigmShift

The US government is inviting inflation with its MMT-tinged policies. Brisk Debt/GDP, M2 increases while retail sales, PMI stage V recovery. Trillions more stimulus & re-opening to boost demand as employee and supply chain costs skyrocket. #ParadigmShift https://t.co/kNT4memOVt pic.twitter.com/Bdw1CDn3Yf

— Cassandra (@michaeljburry) February 20, 2021

“The life of the inflation in its ripening stage was a paradox which had its own unmistakable characteristics. One was the great wealth, at least of those favored by the boom..Many great fortunes sprang up overnight…The cities, had an aimless and wanton youth”

“Prices in Germany were steady, and both business and the stock market were booming. The exchange rate of the mark against the dollar and other currencies actually rose for a time, and the mark was momentarily the strongest currency in the world” on inflation’s eve.

“Side by side with the wealth were the pockets of poverty. Greater numbers of people remained on the outside of the easy money, looking in but not able to enter. The crime rate soared.”

“Accounts of the time tell of a progressive demoralization which crept over the common people, compounded of their weariness with the breakneck pace, to no visible purpose, and their fears from watching their own precarious positions slip while others grew so conspicuously rich.”

“Almost any kind of business could make money. Business failures and bankruptcies became few. The boom suspended the normal processes of natural selection by which the nonessential and ineffective otherwise would have been culled out.”

“Speculation alone, while adding nothing to Germany’s wealth, became one of its largest activities. The fever to join in turning a quick mark infected nearly all classes..Everyone from the elevator operator up was playing the market.”

“The volumes of turnover in securities on the Berlin Bourse became so high that the financial industry could not keep up with the paperwork…and the Bourse was obliged to close several days a week to work off the backlog” #robinhooddown

“all the marks that existed in the world in the summer of 1922 were not worth enough, by November of 1923, to buy a single newspaper or a tram ticket. That was the spectacular part of the collapse, but most of the real loss in money wealth had been suffered much earlier.”

“Throughout these years the structure was quietly building itself up for the blow. Germany’s #inflationcycle ran not for a year but for nine years, representing eight years of gestation and only one year of #collapse.”

His punchline: the above was “written in 1974 re: 1914-1923” and then makes the ominous extrapolation that “2010-2021: Gestation” adding that “when dollars might as well be falling from the sky…management teams get creative and ultimately take more risk.. paying out debt-financed dividends to investors or investing in risky growth opportunities has beaten a frugal mentality hands down.”

We are there now. The only question is when do we enter the exponential currency collapse phase.

Update (1815 ET): one day after the Weimar tweetstorm below, and shortly after our article came out, Burry tweeted the following:

People say I didn’t warn last time. I did, but no one listened. So I warn this time. And still, no one listens. But I will have proof I warned.

Indeed he will.